News and Insights

Ionic Insights: The Business Jet Fleet in Switzerland (May 2023)

To coincide with EBACE 2023 taking place in Geneva next week, this edition of Ionic Insights focuses on Switzerland.

We analyse the size, composition and age of the installed business jet fleet, whilst simultaneously investigating the most popular aircraft registries, OEMs and base locations.

Background

Located at the heart of Europe and with a population of a little under 9 million, Switzerland has the second highest per capita GDP in the world (USD 86,850 as of 2020 - Source: IMF).

Almost three quarters of Swiss GDP is generated by the services sector, with industry generating 25% and agriculture the remaining 1%.

From banks to aircraft maintenance organisations, operators to OEMs (most notably Stans-based Pilatus), Switzerland continues to play a leading role in the business aviation sector.

Analysis

Switzerland boasts a substantial, installed business jet fleet of 150* aircraft (*Source: AMSTAT, May ‘23), nearly forty percent of which are based in the country’s largest city and financial centre of Zurich.

Given Switzerland’s geography and the international footprint of much of the country’s large ultra-high-net-worth community and businesses, Ultra-Long-Range aircraft dominate and in fact represent nearly four out of every ten aircraft.

Dassault is the largest OEM by fleet size, with the Falcon 2000, 7X and 8X models being particularly popular. Cessna (Textron) comes a close second and dominates the Light/Very-Light Jet segment. Contrary to belief, corporate airliners (‘Bizliners’) such as the ACJ and BBJ product lines represent only 3% of all aircraft.

Overall, the average age of the fleet is younger than 12 years; fifty percent of which are registered domestically (HB-).

The largest aircraft operators are Global Jet, Jet Aviation and Albinati Aeronautics.

See the following slide for further information:

Source: AMSTAT, May 2023.

Ionic Aviation will be attending EBACE in Geneva from 23-24 May. We look forward to seeing you there!

Ionic Insights: The Business Jet Fleet in Italy (January 2023)

In this eighth edition of Ionic Insights we focus on Italy. We analyse the size, make-up and age of the installed business jet fleet, whilst simultaneously investigating the most numerous aircraft registries, manufacturers and base locations.

Analysis

With a total of 85* aircraft (Source: AMSTAT, January ‘23), Italy possesses one of the largest business jet fleets in Europe. Approximately two-thirds of all aircraft are based in the north and are concentrated in and around the cultural, financial and automotive hubs of Milan and Turin. Further south, the capital city of Rome is home to 20% of the fleet.

Light/very light and midsize/super-midsize jets dominate. In fact, they represent approximately two-thirds of all aircraft. It is no surprise, therefore, that Cessna (Textron) is the largest OEM by fleet size.

At the other end of the spectrum, ultra-long range aircraft represent only 14% of the fleet; the largest manager of large cabin and ultra-long range jets is Sirio S.p.A. (a subsidiary of Directional Aviation) in Milan.

Overall, the average age of the fleet is 18 years.

Finally, whilst 80% of all jets are registered domestically (I-), it is worth noting that Italy has not yet ratified the Cape Town Convention and self-help remedies are not presently permitted under Italian law.

See a summary in the following slide:

*Source: AMSTAT, January 2023

Ionic Insights: The Business Jet Fleet in the UAE (November 2022)

In the run-up to next month’s MEBAA Show in Dubai, this seventh iteration of Ionic Insights focuses on the United Arab Emirates. We analyse the size, composition and age of the installed business jet fleet, whilst simultaneously investigating the most numerous aircraft registries, operators and base locations.

Market Summary

The UAE has a population of a little over ten million but already boasts the region’s largest fleet of business aircraft. With a total of 108 jets*, the fleet is now twenty-five percent larger than that of its larger neighbour, Saudi Arabia. Over half of all aircraft are based in the business, tourism and cultural hub of Dubai, whilst a quarter are based in the capital city of Abu Dhabi.

The dominant aircraft types are in the ‘heavy’ (ultra-long and corporate airliner/bizliner) segment; these represent over two-thirds of all aircraft.

Whilst Bombardier is the largest OEM by fleet size with 30% of the fleet, it is notable that the Boeing Business Jet (BBJ) product line makes up over one fifth of all aircraft. This includes a total of twenty-four BBJ1, BBJ2, BBJ3, 747, 777 and 787 variants that are operated for the governments of Dubai and Abu Dhabi by Dubai Air Wing and Presidential Flight respectively, and Royal Jet.

Unsurprisingly, light jets make up less than 6% of the fleet. The largest owner-operator of light jets is Emirates Flight Training Academy in Dubai, with a total of five Embraer Phenom 100EV aircraft. Interestingly, the Cessna Citation product line does not currently feature.

Overall, the average age of the fleet is 13 years; whilst a little under half of all aircraft are registered domestically, A6.

Opportunities for Financing

The financing of bizliners, particularly widebodies, for UHNW clients is most commonly driven by a handful of international private banks who do so on the basis of a client’s wider wealth relationship. That being said, asset and credit-based solutions exist for narrowbody variants such as BBJs, ACJs and the Embraer Lineage, albeit at more conservative advances and with faster amortisations than might otherwise be available for other new and pre-owned business aircraft.

A summary of the fleet is included in the following slide:

*Source: AMSTAT, Nov 22

Ionic Insights: The Business Jet Fleet in Nigeria (September 2022)

In this sixth edition of Ionic Insights we focus on Nigeria. We analyse the size, make-up and age of the installed business jet fleet, whilst simultaneously investigating the most numerous aircraft registries, manufacturers and base locations.

Market Summary

With over 200 million citizens Nigeria has the largest population and economy in Africa. The country produces over 2% of the world’s oil; but whilst it now represents a relatively small part of the country’s overall economy, Nigerian government revenues are still heavily dependent on the sector. In addition, the oil industry has driven the growth and expansion of its large fleet of 119* helicopters.

With respect to business jets, Nigeria boasts an installed fleet of 80* aircraft and is second only to South Africa in Africa in terms of overall size. Bombardier is the largest OEM with 34% of the fleet. Legacy Hawker-Beechcraft equipment makes up 28%, and Embraer 14%.

The dominant aircraft categories are the mid/super-midsize and large cabin segments; with the average age of the fleet being 18 years. Not surprisingly, nearly two thirds of all aircraft are based in Lagos, Nigeria’s largest city and the country’s financial, economic and cultural hub.

Business Jet Financing

Whilst domestic sources of finance are available, securing competitive aircraft financing by international asset and credit-based lenders and private banks (e.g., those requiring assets under management or ‘AUM’) remains challenging, but is by no means impossible. The hurdles are however not insubstantial – the country currently ranks 154 out of 180 on Transparency International’s Corruption Perceptions Index; internal security remains an issue; and two thirds of the fleet is registered domestically (5N).

Credit, jurisdictional risk and registration aside, the willingness of owners to retain, via tripartite agreement with lender, the services of an experienced and independent aircraft management company (such as ACASS, ANAP Jets, Empire Aviation, Execujet or Skyjet, amongst others) in the day-to-day management and operation of their aircraft is a standard requirement of those willing to finance aircraft there.

This analysis is summarised in the following slide:

*Source: AMSTAT, Sep 22

Ionic Insights: The Installed Business Jet Fleet in Australia (August 2022)

In this, our fifth edition of Ionic Insights we focus on Australia. We analyse the size, make-up and age of the installed fleet, whilst simultaneously investigating the most numerous aircraft registries and base locations.

Analysis

Being the sixth largest country in the world by land mass, Australia has a relatively large installed fleet of 226 aircraft.

Despite having an economy only one tenth of the size and a population one fiftieth of that of its largest trading partner, China, the installed fleet is only 7% smaller.

The presence of many large domestic and multinational corporations, particularly in the mining, agricultural and financial services sectors, drives the ownership of heavy, ultra-long-range aircraft at the top end. It is not surprising therefore that two-thirds of these aircraft are based in the financial centres of Sydney and Melbourne; whilst over a third of all aircraft are based in Sydney (Australia’s most populous city) and New South Wales alone.

The dominant aircraft category is the Light/Very-Light Jet segment – which represents around two thirds of the overall market. Cessna is the largest OEM by fleet size with approximately 37% of the fleet; Bombardier (including Learjet) is in second with 35%.

The prevalence of large numbers of Light/Very-Light aircraft (and their resultant small deal sizes) means that the opportunities for attracting international, cross-border financing are comparatively limited. However, the strong overall economy, English common law-based legal system and the presence of independent aircraft management companies (ExecuJet Australia being the largest) are strong positives for those financing larger aircraft.

The average age of the fleet is twenty-two years; and whilst nearly nine out of every ten aircraft are registered in Australia (VH-), the remainder are registered in the U.S., with a single aircraft being registered in the Cayman Islands (VP-C).

This analysis is summarised in the following slide:

The Installed Business Jet Fleet in Australia, August 2022.

Ionic Insights: The Installed Business Jet Fleet in the United Kingdom (June 2022)

To coincide with the return of this month’s Farnborough International Airshow, this edition of Ionic Insights focuses on the United Kingdom. We analyse the size, make-up and age of the installed fleet, whilst simultaneously investigating the most numerous aircraft operators, registries and base locations.

Analysis

With an installed fleet of 209 aircraft, the UK is second only to Germany in Europe in terms of numbers of aircraft and is broadly similar in scale to that of France. Bombardier is the largest OEM by fleet size (28%), with Cessna (22%) and Dassault (15%) being not far behind.

The dominant aircraft categories are the Mid/Super-Midsize and Ultra-Long-Range segments – each boasting around a third of overall market share. In addition, Light/Very-Light jets make up approximately one quarter of the fleet.

Overall fleet size and composition is heavily influenced by the presence of an extensive commercial airline network plus the relatively compact geography of the UK and Western Europe; the presence of a large UHNW community and many multinational corporations drives ownership of ultra-long-range aircraft at the top end.

Not surprisingly, nearly half of all aircraft are based in the London area; with Jet Concierge, Luxaviation UK (formerly LEA), TAG, GAMA and Catreus being the largest operators.

Over 50% of aircraft are registered domestically in the UK (G-), with the Isle of Man (M-), U.S. (N) and the Channel Islands (2-) being the most popular registries thereafter.

This analysis is summarised in the following slide:

Figure: The Installed Business Jet Fleet in the United Kingdom

Upcoming Events

Ionic Aviation will be attending the Farnborough Airshow from 18 – 20 July.

Ionic Aviation to attend EBACE 2022

Ionic Aviation will be attending the European Business Aviation Convention and Exhibition (‘EBACE’) in Geneva, Switzerland, from 23-25 May 2022.

EBACE is Europe’s premier gathering of business aviation professionals and attracts aircraft owners, original equipment manufacturers, advisers and other industry participants from all over the world.

Reach out to us directly if you are attending and would like to meet.

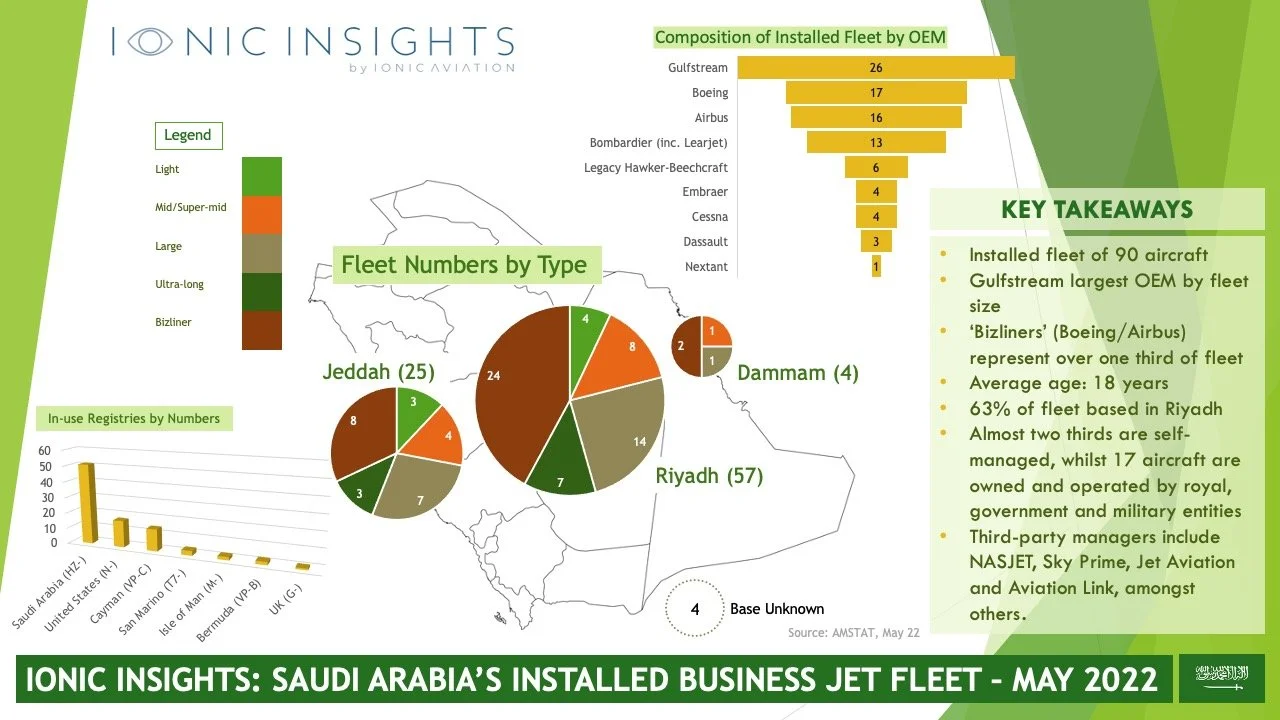

Ionic Insights: The Installed Business Jet Fleet in Saudi Arabia (May 2022)

In this third edition of Ionic Insights, our regular country by country spotlight on the global business aviation sector, we focus on the Kingdom of Saudi Arabia. We analyse the size, make-up and age of the installed fleet, whilst simultaneously investigating the most numerous aircraft registries and base locations.

Historically the Middle East’s largest business aviation market, the installed fleet in Saudi Arabia is now smaller than that of the UAE. This is down to several factors, but the continued relocation of many multinationals and ultra-high-net-worth individuals to the Emirates, plus the fallout from 2017’s Riyadh ‘Ritz-Carlton Prison’ episode are key.

Saudi Arabia has an installed fleet of 90 aircraft*, with Gulfstream being the largest OEM by fleet size (29% of the fleet). Perhaps unsurprisingly, corporate variants of commercial aircraft – notably ‘bizliners’ manufactured by Boeing and Airbus – represent over one third of the entire base. Almost two thirds of aircraft are based in Riyadh, the political and administrative capital.

In a challenge to those seeking to finance/refinance aircraft within the Kingdom, almost two thirds of aircraft are self-managed (no third-party operator involvement), 57% are registered locally in Saudi Arabia (HZ-), and a total of 17 aircraft are owned and operated by a variety of royal, government and military entities.

The key takeaways from this analysis are summarised in Figure 1 below.

If you found this information interesting, feel free to sign up to receive future editions direct to your Inbox via the pop-up notification on this website.

Figure 1: A summary of the installed fleet in Saudi Arabia. *Source: AMSTAT, May 22

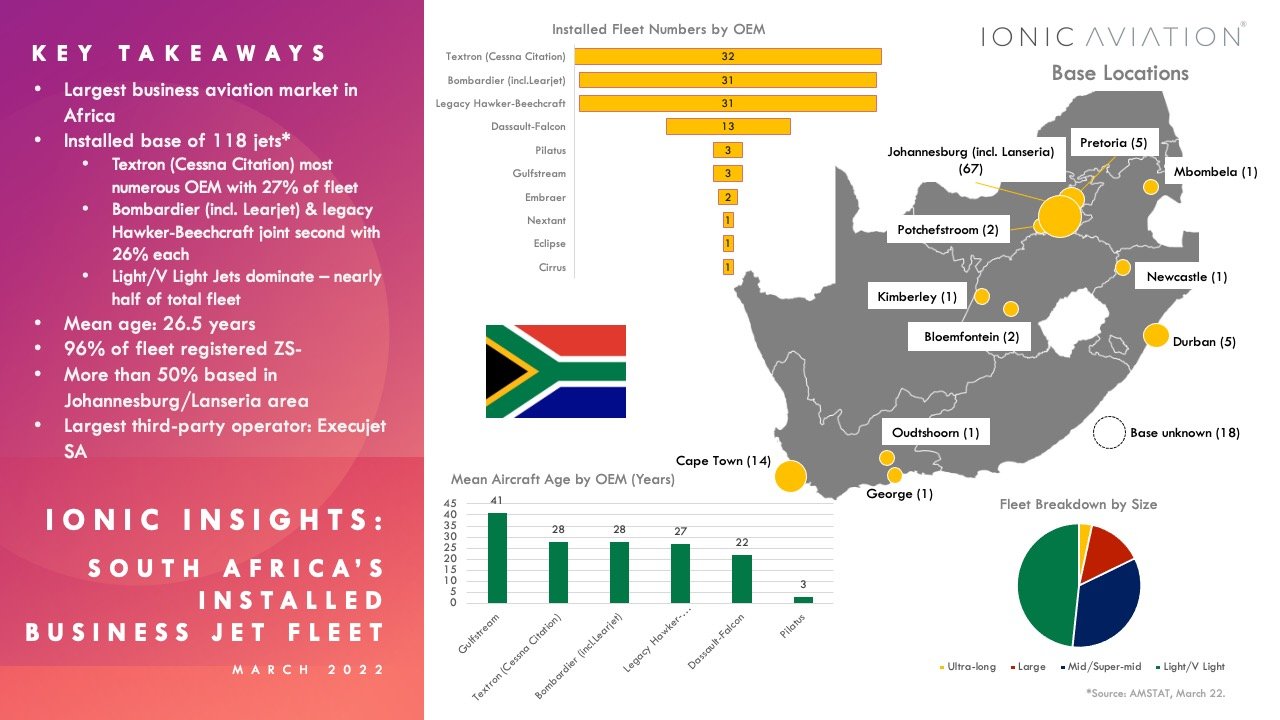

Ionic Insights: The Installed Business Jet Fleet in South Africa (March 2022)

Welcome to the second edition of Ionic Insights, our new and regular focus on the global business aviation sector.

Each Insight serves to provide financiers, investors, brokers and other interested parties an easily digestible snapshot of the installed business jet fleet within a specific country or region.

In this edition we focus on South Africa. We analyse the size, makeup and average age of the installed fleet, aircraft registries and base locations.

Whilst the size of the fleet is dwarfed by the number of helicopters and turboprops in operation – jets represent only one third the number of helicopters and approximately one half the number of turboprops – South Africa boasts more jets than any other market in Africa.

The market is biased towards the lighter, smaller end of the market; with the vast majority of such aircraft being self-managed. The national registry (ZS-) is almost entirely dominant. Whilst the mean age of the fleet is comparatively old at over twenty-six years, it is notable that less than 2% of that fleet is listed for sale – almost half the current global average.

I hope you find this Insight useful. Look out for future editions!

A summary of the installed business jet fleet in South Africa, March 2022.

Ionic Insights: The Installed Business Jet Fleet in Ukraine (January 2022)

Given the scale of the challenges faced by aviation over the past two years, the last thing the industry needs is war in Ukraine.

Whilst conflict remains unlikely, the ongoing rhetoric and build-up of military forces means that the potential for misunderstanding and mistakes is high. In addition to the obvious consequences for the people of Ukraine, there are significant concerns about the likely impact of military action upon freedom of navigation, flight safety, security of and access to civilian airfields, and the resultant disruption to commercial airline networks.

Given that over forty percent of the installed base is self-managed, and a significant portion of the fleet is in the very-light/light and mid/super-midsize categories (including six out-of-production Hawker aircraft), the potential for large numbers of banks and financiers being impacted is low. However, for those that are it would be surprising if Risk and Asset Management staff hadn’t already begun the process of considering the location, security, and technical condition of their aircraft and hard-copy records, and the suitability of their borrowers’ insurance coverage.

Conflict or no conflict, it goes without saying that the impact of all of this upon the appetite of financiers to consider future aircraft lending in Ukraine (and other European nations near Russia) is yet to be fully understood; however, it is unlikely to be particularly helpful.

In this first in a series of country-specific studies, we investigate the size and nature of the installed base, the market’s leading management companies and operators, aircraft registries, and the habitual bases of the aircraft.

A summary of the installed business jet fleet in Ukraine, January 2022.